December 2025 Quarterly Activities Report

By LSE RNS

Date: Thursday 22 Jan 2026

22 January 2026

Q4 2025 Activities Report

For the Quarter ending 31 December 2025 ('Q4', 'December Quarter' or 'the Quarter')

|

Quarterly Highlights

• Total Recordable Injury Frequency Rate (TRIFR) decreased to 1.87 from 1.95 at the end of December 2025 with only four recordable injuries during the Quarter

• Group gold production of 65,918 ounces (oz) (Q3 2025: 59,857oz) meeting expectations due to continued stockpile processing at Mako (Senegal) and improved underground output at Syama (Mali)

• All-In Sustaining Costs (AISC) of $1,877/oz(Q3 2025: $2,205/oz) in line with expectations as higher gold production partially offset higher royalty payments

• Quarterly capital expenditure (excluding exploration) of $18.4 million (Q3 2025:$26.6 million) in line with expectations consisting of $16.0 million non-sustaining and $2.4 million of sustaining capital

• Q4 operating cash flow generation of $85.7 million(Q3: $67.8 million) (operating cash flow before capital expenditure, exploration and working capital)

• Updated Doropo (Côte d'Ivoire) Definitive Feasibility Study (DFS) outlined larger, longer-life operationwith LOM average production of c. 170kozpa over 13 years and a post-tax project NPV5% of US$1.46bn, IRR of 49% (at $3,000/oz gold price)

• Net cash of $209.1 million(Q3 2025: $136.6 million), including cash, cash equivalents and bullion of

$266.0 million. Drawn overdraft balances and equipment financing were $57.0 million; Group available liquidity of $322.3 million

• La Debo (Côte d'Ivoire) Mineral Resource Estimate (MRE) of 17.6 Mt grading 1.14 g/t Au for 643 koz of contained gold - 60% larger than historical estimates

• Encouraging results from drilling at ABC Project (Côte d'Ivoire) targeting extension of existing MRE including 9m at 2.4 g/t Au from 0m and 23m at 2.1 g/t Au from 81m

Full-Year Highlights

• Group gold production of 277,236 oz (2024: 339,869oz) at AISC(1) of $1,843/oz (2024: 1,476oz) within guidance

• Gold sales of 258,544 oz at an average realised price of $3,338/oz (2024: 335,708oz at $2,383/oz) generating gold revenue of $865.6 million (2024: $664.1 million)

• Capital expenditure (including exploration) of $117.5 million (2024: $96.3 million) was within guidance ($109 - 126 million), including $3.0 million at Mako, $84.5 million at Syama and $24.1 million on exploration

• Operating cash flow generation of $313.5 million(2024: $249.0 million) (operating cash flow before capital expenditure, exploration and working capital)

• EBITDA1 of $382.9 million (2024: $287.6 million).

2026 Guidance

• Group production guidance of 250,000 - 275,000 oz at a Group AISC of $2,000 - 2,200/oz

• Group capital expenditure of $310- 360 million,including Doropo Project capital and Exploration of

$170 - 190 million and $15 - 25 million respectively

• Mako guidance of 55,000 - 65,000 oz at an AISC $1,600 - 1,800/oz; full-year of stockpile processing

• Syama guidance of 195,000 - 210,000 oz at an AISC $1,950 - 2,150/oz with full ramp-up of the Syama Sulphide Conversion Project (SSCP) expected in H2

• Construction at Doropo expected to commence in H1 2026 upon receipt of permits and full FID; early works and procurement of long-lead items are ongoing in order to achieve first gold pour in H1 2028

Note: Unless otherwise stated, all dollar figures are United States dollars ($). AISC guidance is based on $4,000/oz gold price.

|

Resolute Mining Limited (Resolute, the Company or the Group) (ASX/LSE: RSG), the West Africa-focused gold miner, is pleased to present its Quarterly Activities Report for the period ended 31 December 2025.

Chris Eger, Chief Executive Officer, commented,

"2025 has been a robust and transformational year for Resolute, marked by strategic asset growth and a significantly strengthened financial position. Despite supply chain challenges in Mali and the transition to stockpile processing at Mako, we have achieved strong financial and operating performance. Gold production was in-line with initial guidance and net cash generation over the year was $140m driven by a very strong Q4. We advanced key projects such as the SSCP and Mako Life Extension Project (MLEP), managed operating costs across all sites, restructured the executive teams, delivered exploration success and stabilized government relations.

We also successfully acquired the Doropo and ABC Projects in Côte d'Ivoire. The team have been advancing these projects whilst simultaneously adding value to them. Doropo remains on track for first production in the first half of 2028. This project is a key component of the Company's strategy to become a more diversified gold producer, expanding across multiple assets and countries to achieve an annual production target of over 500 koz by the end of 2028. We plan to commence construction of Doropo leveraging our strong balance sheet and net cash position of over $200 million as a solid foundation for the project.

Importantly, as a business we have responded proactively to changing operational dynamics in Mali and have achieved full-year production of 277 koz in-line with our guidance set out at the start of the year.

In Q4, we confirmed the exceptional economics of Doropo with robust margins, a long 13-year mine life and over 170koz of annual gold production. Doropo will drive significant growth for Resolute and deliver substantial benefits to Côte d'Ivoire's communities. Our strong relationship with the Ivorian authorities

|

1 EBITDA is a non-GAAP measure that has not been audited and represents earnings before interest, taxation, depreciation and amortisation.

and continued progress this year ensure we remain on track for construction to begin in the first half of 2026.

For 2026 we expect group production to be between 250,000 - 275,000 oz of gold at between $2,000 - 2,200/oz AISC. The lower production in 2026 is a result of stockpile processing at Mako (55 - 65 koz) and commissioning and ramp up of the SSCP at Syama (195 - 210 koz). The increased AISC costs are a consequence of higher royalty expenses in the higher gold price environment and the expected reduced gold production.

Looking ahead to 2026, our strategic priorities will centre on the commissioning of the SSCP, marking a critical step in strengthening our Mali operations. The SSCP's aim is to increase overall sulphide processing capacity at Syama by over 60% from 2.4 Mtpa to 4.0 Mtpa by modifying the oxide comminution circuit and upgrading the roaster. The project is important for the long-term future of Syama as oxide resources deplete and the ore sources become predominantly sulphide. Importantly, the SSCP will retain operational flexibility by maintaining the ability to switch back to treat oxide ore as needed.

Another key workstream in 2026 is the ramp up of construction at Doropo, bringing the project closer to first production and advancing our growth ambitions in Côte d'Ivoire. Meanwhile, in Senegal, we will continue to progress technical studies for the MLEP - a project focusing on developing two near-mine satellite deposits (Tomboronkoto and Bantaco) that will provide new ore to the existing Mako plant and ensuring the asset's long-term value.

Exploration remains at the heart of Resolute's strategy, underpinning our ambition to deliver sustained growth and maximize long-term shareholder value. In 2025, the Company achieved several key milestones, including updated reserves at Doropo, initial resources at Bantaco and resource upgrades at La Debo. These successes highlight the effectiveness of our ongoing organic exploration programs, which are focused on expanding the Group's resource base, extending mine life, and identifying new high-value targets within our portfolio. In the robust gold price environment, our commitment to exploration is stronger than ever, as we recognize its critical role in driving organic growth and enhancing asset value. We have also made strategic moves to secure future growth by acquiring new permits in Côte d'Ivoire and are actively pursuing additional permit opportunities in Guinea. In addition, we anticipate providing further updates on exploration and mine extension activities in Senegal before year-end, reinforcing our dedication to discovery and development as catalysts for future value creation. Through disciplined investment in exploration, Resolute is well positioned to unlock new opportunities and deliver lasting benefits to shareholders and host communities alike.

With a strong balance sheet and disciplined execution, we are poised to build upon this year's achievements and deliver sustained growth and value for all stakeholders."

Webcast and Conference Call

Resolute will host a conference call for investors, analysts, and media on 22 January 2026, to discuss the Company's Quarterly Activities Report for the period ending 31 December 2025 and provide 2026 guidance. This call will conclude with a question-and-answer session.

Conference Call: 8:00pm (AEDT, Sydney) / 9:00am (GMT, London)

Webcast registration link: https://sparklive.lseg.com/ResoluteMiningLtdAustralia/events/75a06fbf-d314-4e1a-bd6e-d6153e28f868/resolute-mining-q4-2025-activities-and-2026-guidance

Those wishing to ask questions as part of the Q&A should use the conference call facility (please join five minutes prior to the start time).

Conference call registration link: https://registrations.events/direct/LON34665210

A presentation, to accompany the call, will be available for download on the Company's website: https:// www.rml.com.au/investors/presentations/.

Group Operations Overview

December |

September |

December |

Full Year |

Full Year | |

2025 | 2025 | 2024 | 2025 | 2024 | |

Group Summary Units | Quarter | Quarter | Quarter | YTD | YTD |

Mining | |||||

Ore Mined t | 858,470 | 672,177 | 1,583,820 | 4,250,959 | 6,274,965 |

Mined Grade g/t | 2.14 | 2.10 | 1.93 | 2.04 | 2.06 |

Processing | |||||

Ore Processed t | 1,581,115 | 1,520,742 | 1,651,031 | 6,209,834 | 6,156,602 |

Processed Grade g/t | 1.51 | 1.48 | 1.93 | 1.65 | 2.01 |

Recovery % | 84 | 82 | 85 | 84 | 86 |

Gold Poured oz | 65,918 | 59,857 | 87,687 | 277,236 | 339,869 |

Sales | |||||

Gold Sold oz | 49,941 | 63,483 | 83,145 | 258,544 | 335,708 |

Avg Realised Price $/oz | 4,023 | 3,404 | 2,659 | 3,338 | 2,383 |

Financials | |||||

Capital Expenditure $m | 18.4 | 26.6 | 25.3 | 87.4 | 96.3 |

Net (Cash) $m | (209) | (137) | (66) | (209) | (66) |

AISC $/oz | 1,877 | 2,205 | 1,568 | 1,843 | 1,476 |

Table 1: Resolute Group Operational Performance Summary

During the Quarter, Resolute processed over 1.58 Mt across Syama (Mali) and Mako (Senegal) at an average milled head grade of 1.51 g/t. In Q4 the Group produced 65,918 oz of gold at an AISC of

$1,877/oz.

Environmental and Social Update

Resolute's TRIFR as of 31 December 2025 was 1.87 (Q3 2025: 1.95) with four recordable injuries during the Quarter. This is below the industry (ICMM) average benchmark of 2.29 in 2024. In Q4, Resolute recorded no significant environmental incidents, regulatory non-compliances, nor reportable community grievances.

During the Quarter, the Board of Directors reviewed and approved amendments to Resolute's corporate governance framework comprising Board Charters and policy documents. This included a general update to the existing Sustainability Committee Charter and ESG policies, and the introduction of a new Energy and Climate Change Policy.

Resolute's draft FY25 Climate Report including GHG emissions inventory was presented to the Board of Directors for advanced feedback before scheduled publication in Q1 2026. These climate-related disclosures have been prepared in accordance with the Australian Sustainability Reporting Standards (ASRS).

Resolute has re-engaged Bureau Veritas to audit conformance against ISO 14001 Environmental Management and 45001 OHS Management standards. A conformance audit was completed at the Mako mine during the Quarter, with an audit of the Syama mine to follow in H1 2026.

Under the scope of its Biodiversity Offset Programme, the Mako mine hosted a site visit and bi-annual meeting of its independent Advisory Panel. The Advisory Panel has provided oversight to the implementation of the Biodiversity Offset Programme at Mako for the past 10 years.

Mali

Syama Operations

Syama gold production for the Quarter was 47,163oz at an AISC of $1,779/oz. The operational performance is set out in the table below.

|

Summary |

Units | December 2025 Quarter | September 2025 Quarter | December 2024 Quarter | Full Year 2025 YTD | Full Year 2024 YTD |

Mining | Sulphide | ||||||

Ore Mined | t | 711,984 | 490,154 | 562,996 | 2,205,298 | 2,400,714 | |

Mined Grade | g/t | 2.20 | 2.25 | 2.50 | 2.30 | 2.56 | |

Oxide | |||||||

Ore Mined | t | 146,486 | 182,023 | 248,082 | 803,650 | 806,036 | |

Mined Grade | g/t | 1.83 | 1.70 | 1.58 | 1.53 | 1.58 | |

Processing | Sulphide | ||||||

Ore Processed | t | 582,931 | 614,262 | 661,208 | 2,360,251 | 2,404,832 | |

Processed Grade | g/t | 2.34 | 2.08 | 2.55 | 2.25 | 2.64 | |

Recovery % | 78 | 75 | 77 | 76 | 79 | ||

Gold Poured | oz | 35,998 | 31,833 | 43,863 | 135,436 | 163,379 | |

Gold Sold | oz | 18,861 | 37,419 | 42,247 | 119,780 | 162,032 | |

Oxide | |||||||

Ore Processed | t | 394,486 | 349,494 | 417,768 | 1,568,595 | 1,522,976 | |

Processed Grade | g/t | 1.02 | 0.91 | 1.27 | 0.98 | 1.24 | |

Recovery % | 81 | 79 | 88 | 82 | 86 | ||

Gold Poured | oz | 11,165 | 8,085 | 15,021 | 40,905 | 52,555 | |

Gold Sold | oz | 11,165 | 8,085 | 15,021 | 40,905 | 52,555 | |

Cost | Syama combined | ||||||

Capital Expenditure | $m | 18.1 | 26.0 | 22.5 | 84.5 | 81.1 | |

AISC | $/oz | 1,779 | 2,358 | 1,525 | 2,008 | 1,497 | |

Table 2: Syama Production and Cost Summary

Total gold poured at Syama of 176,341 oz in 2025 was 18% lower than the prior year as head grades at both sulphide and oxide plants were lower due to slightly lower mined grades and increased use of stockpiled material. Both plants maintained high utilisation and operated near nameplate capacity of

3.9Mt. The combined ore tonnes mined marginally decreased to 3.0 Mt (vs 3.2 Mt in 2024) due to approximately 0.2Mt less sulphide ore being mined in the sub-level cave due to disruption of explosive supplies which the Company has been addressing since Q3. Explosive supplies are not expected to be a major issue moving forward as an emulsion plant is planned to be built on site in 2026.

Q4 was a strong Quarter, with 47,163 oz of gold poured at across the sulphide and oxide operations. Ore production from the underground operation improved to its highest level in 2025, as the impact of supply chain disruptions were minimised due to measures put in place in the prior Quarter. Higher mined grade from the underground resulted in improved head grade in the sulphide plant as less

stockpile material was blended. In Q4 the oxide operation performed in line with expectations with a higher proportion of higher-grade run of mine ore being processed along with lower grade stockpiles.

The full-year AISC at Syama of $2,008/oz was 25% higher than in 2024 ($1,497/oz) and was within revised guidance ($1,900 - 2,050). The increase in AISC in 2025 is mainly attributed to increased royalty payments as well as a reduction in gold poured compared to the prior year. In Q4 2025 the AISC decreased to $1,779/oz due to increased production and cost reductions as part of the ongoing work to optimise the Syama operation.

Full-year capital expenditure was $84.5 million including $23.9 million of expenditure on the SSCP project, $22.2 million on capitalised waste and $38.4 million on capital projects which include mining heavy vehicles, the roaster upgrade and design changes to the TSF. During Q4 2025 capital expenditure was $17.9 million split $1.9 million and $16.0 million between sustaining and non-sustaining capital respectively. Expenditure for the Quarter includes roaster upgrades, truck upgrades and security fencing in Syama and Tabakoroni, with $4.7 million spent on the SSCP as well as $0.3 million of sustaining waste capital.

Senegal

Mako Operations

Mako gold production for the Quarter was 18,755oz at an AISC of $1,666/oz. The operational performance for Mako is set out in the table below.

| December | September | December | Full Year | Full Year | |

Summary |

Units | 2025 Quarter | 2025 Quarter | Quarter | 2025 YTD | 2024 YTD |

Mining | ||||||

Ore Mined | t | - | - | 772,742 | 1,242,012 | 3,068,215 |

Mined Grade | g/t | - | - | 1.63 | 1.91 | 1.80 |

Processing | ||||||

Ore Processed | t | 603,698 | 556,986 | 572,055 | 2,280,987 | 2,228,793 |

Processed Grade | g/t | 1.04 | 1.18 | 1.69 | 1.49 | 1.86 |

Recovery | % | 91 | 91 | 92 | 92 | 93 |

Gold Poured | oz | 18,755 | 19,939 | 28,803 | 100,895 | 123,935 |

Gold Sold | oz | 19,915 | 17,979 | 25,877 | 97,859 | 121,121 |

Financials | ||||||

Capital Expenditure | $m | 0.3 | 0.6 | 2.8 | 2.9 | 15.2 |

AISC | $/oz | 1,666 | 1,415 | 1,350 | 1,270 | 1,244 |

Table 3: Mako Production and Cost Summary

Full-year gold production of 100,895 oz exceeded expectations and was within the revised guidance range (98-102koz). Gold production in 2025 was expected to be lower than the prior year as open pit mining ceased in Q2 2025 and the operation transitioned to stockpile processing during the second half of 2025.

During Q4 the plant continued to process stockpile material. Gold production of 18,755 oz was driven by stockpile grades that remained higher than expected.

The full-year AISC at Mako of $1,270/oz for 2025 was marginally higher than 2024 ($1,244/oz) and below original guidance ($1,300 - 1,400/oz). The small increase in AISC in 2025 is mainly attributed to increased royalty payments due to higher gold prices as well as lower gold production as the operation transitioned to stockpile processing.

In Q4 2025 the AISC increased to $1,666/oz due to lower gold production from stockpile processing and higher royalties due to the gold price environment. Included in the AISC in the Quarter is approximately $143/oz of non-cash stockpile movements.

Full-year capital expenditure at Mako was $2.9 million (2024: $15.2 million) with no waste stripping or major capital items required. In Q4 capital expenditure was $0.3 million (Q3 2025: $0.6 million) and consisted of on-going activities for the final Tailings Management Facility raise as well as replacement parts for the processing plant.

Mako Life Extension Project

Tomboronkoto and Bantaco are two potential satellite deposits that Resolute is advancing in order to extend the life of the Mako Mine. These are collectively referred to as the Mako Life Extension Project ("MLEP").

The current combined Mineral Resource Estimates of Tomboronkoto and Bantaco contain over 600 koz of gold, with possibilities of expansion based on ongoing exploration results.

In Q4 $4.1 million was spent on the MLEP primarily consisting of drilling at Bantaco.

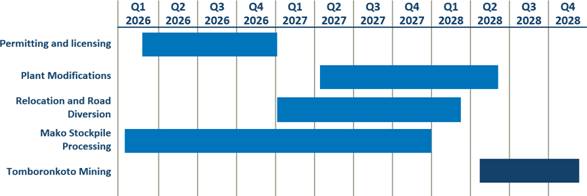

Tomboronkoto

The Environmental & Social Impact Assessment (ESIA) report has been pre-validated by technical agencies in advance of ministerial approval. Detailed planning and survey activities are ongoing in consultation with potentially affected persons for the resettlement of Tomboronkoto village located proximal to the deposit.

The application for a Mining Permit will follow the issuance of the Environmental Permit and is targeted for Q1 2026. the Mining Permits is anticipated to be received, assuming no major revisions, by the end of 2026.

Planning and stakeholder engagement activities to inform the development of the Resettlement Action Plan (RAP) are already underway and remain ongoing. The receipt of the Mining Permit will provide the necessary authority to implement the RAP, including the initiation of village relocation, once agreement has been reached with affected parties. This approach underscores our commitment to regulatory compliance, transparent community consultation, and responsible project execution.

Formal EIA studies for the expansion of the existing Mako Mine process plant including a new Tailings Storage Facility are ongoing. In 2026, detailed engineering is expected to start in the second half of year.

Figure 1: Approximate Timeline for Tomboronkoto

Bantaco

In Q4 the main activities included infill drilling at the Bantaco South prospect, metallurgical test work, progression of technical studies, commencement of the ESIA and community engagement activities.

In 2026 the key workstreams are related to completing technical studies, infill drilling and permitting.

Senegal Exploration

During Q4, infill drilling at Bantaco South and West Prospects, aimed at converting inferred resource to indicated, was completed in December 2025.

An update of the MRE is underway for both Bantaco West and Bantaco South with the results expected in H1 2026.

Côte d'Ivoire

Doropo Project

The Doropo Project is in the northeast of Côte d'Ivoire in the Bounkani region, 480 km north of the capital Abidjan and 50 km north of the city of Bouna. Resolute acquired the asset in May 2025 and since then has updated the Resource, hired the project team (Rob Cicchini as Project Director), started community engagement, progressed permitting and updated the DFS.

The updated DFS, released on 15 December 2025, confirms Doropo as a long-life, high-margin asset capable of materially expanding Resolute's annual production base to over 500 koz by the end of 2028. First gold is targeted for H1 2028, with construction expected to begin in H1 2026 following the expected receipt of the Mining Permit and FID.

The government maintains strong commitment in support of the Doropo Project following publication of the optimised DFS. Detailed community land and asset surveys commenced within potentially affected areas, in preparation for the commencement of early works construction activities in H2 2026.

Activities in Q4 2025 included receiving bids for the early earth works tender and issuing the tender for the Engineering, Procurement and Construction Management (EPCM) Contract. During the Quarter, the front-end engineering design (FEED) contract was awarded to Lycopodium and the building of the Owners team commenced.

Updated DFS Summary

The updated DFS outlines a significantly larger project, increasing total ore reserves by ~55% to 59.1 Mt at 1.31 g/t for 2.50 Moz of contained gold, driven primarily by a higher reserve price assumption of

$1,950/oz (vs. $1,450/oz previously). This expands the mine life to 13 years (from 10) and increases total life of mine (LOM) production to 2.2 Moz.

The operating and financial highlights at a $3,000/oz gold price are included in the table below.

Units | Value | |

Mine Life | Years | 13 |

LOM ore processed | kt | 59,102 |

LOM strip ratio | w:o | 4.9 |

LOM feed grade processed | Au g/t | 1.31 |

LOM gold recovery | % | 88 |

LOM gold production | koz | 2,196 |

Upfront capital cost | US$M | 516 |

Life of Mine average: | ||

Gold, average annual production | koz | 169 |

Cash costs per ounce | US$/oz | 1,123 |

AISC per ounce | US$/oz | 1,406 |

EBITDA | US$M | 294 |

Free Cash Flow (post-tax) | US$M | 214 |

Project years 1 to 5:

Gold, average annual production | koz | 204 |

Cash costs per ounce | US$/oz | 1,005 |

AISC per ounce | US$/oz | 1,294 |

EBITDA | US$M | 364 |

Free Cash Flow (post-tax) | US$M | 268 |

Pre-Tax Economics | ||

Net present value - 5% | US$M | 1,959 |

Internal Rate of Return | % | 57 |

Post-Tax Economics

Net present value - 5% US$M 1,457

Internal Rate of Return % 49

Payback period (from first production) Years 1.7

Table 4: Doropo DFS Highlights

Average annual LoM production is estimated at ~170 koz. Gold production is higher in the first five years with average annual gold production of 204koz. The average gold recovery is estimated at 88% over the LOM. The production schedule is anchored by the Souwa "hub" region and Kilosegui, supplemented by multiple satellite pits early in the mine life.

Upfront capital cost is estimated at $516 million, reflecting a larger processing plant (fresh ore capacity has increased from 4.0 Mtpa to 4.9 Mtpa), updated pricing, and inclusion of previously omitted items. Operating costs have also been revised to market conditions as at the end of 2025, increasing in the average AISC over the LOM to $1,406/oz.

At a base case gold price of US$3,000/oz, Doropo deliver a post-tax NPV5% (100% basis) and IRR of

$1.5 bn and 49% respectively. Higher gold production in the first five years results in a payback period of 1.7 years from the start of production. At a gold price of $4,000/oz and $4,500/oz the post-tax NPV5% (100% basis) increases to c. $2.5 bn and c. $3.1 bn respectively.

Plans for 2026

In Q1 the target is to complete FEED and, award the EPCM contract. As part of the FEED tenders for equipment and construction packages with be prepared and issued. The main focus of the FEED in Q1 will be to advance long lead items and prepare the site for construction activities. This will include tendering key long lead items and construction contracts.

In parallel, the Resolute owner's team is running a competitive bid process for the EPCM contract for the Doropo Project. Engineering companies with a proven track record in delivering gold projects in West Africa have been invited with tenders expected to be received in Q1. Adjudication will continue throughout the Quarter with formal award planned in Q2.

Resolute expects to receive the mining permit shortly. Upon receipt of the mining permit, resettlement and livelihood programs will advance.

Assuming FID is completed by the end of Q1, capital expenditure at Doropo is expected between $170 - 190 million in 2026. Expenditure is expected to be weighted (75%) towards H2 and includes the following workstreams:

• Commence works on the construction camp and village

• Commence earthworks for water storage and the water harvesting dam

• Plant site and village earthworks

• Award EPCM contract

• Continue building owners team

• Land acquisition and crop compensation

• Procurement of long-lead items and steelwork fabrication

• Appoint engineer, start detailed design and procurement activities for the HV grid power

Next Steps

Resolute continues to await approval of the Mining Permit by the Interministerial Commission. This is followed by signing of the Presidential Decree. This is expected in the next month.

Once the mining permit is received, Resolute will proceed with FID. With strong cash flows from Syama and Mako, available liquidity of over $320 million, access to local and international capital, a strong project team, and established government and community relationships, we are confident all necessary elements are in place to move forward.

Côte d'Ivoire Exploration

ABC Project

The ABC Project is a greenfield exploration project located in western Cote d'Ivoire. Resolute has four exploration permits granted around the ABC Project with two further permit applications.

Over Kona North and South deposits there is a NI 43-101-compliant Inferred MRE of 2.16 Moz grading

0.9 g/t Au contained within the Kona permit.

During Q4 a focused reverse circulation (RC) drilling program was completed across the Farako-Nafana and Kona permits to test priority gold targets generated from integrated surface geochemistry (soil & termite mound sampling), geological mapping, pXRF multi-element analysis and geophysical interpretation.

Drilling at the Yele prospect (Figure 5) intersected 31m grading 2.4 g/t from 13m, highlighting the prospect as a priority for follow-up drilling.

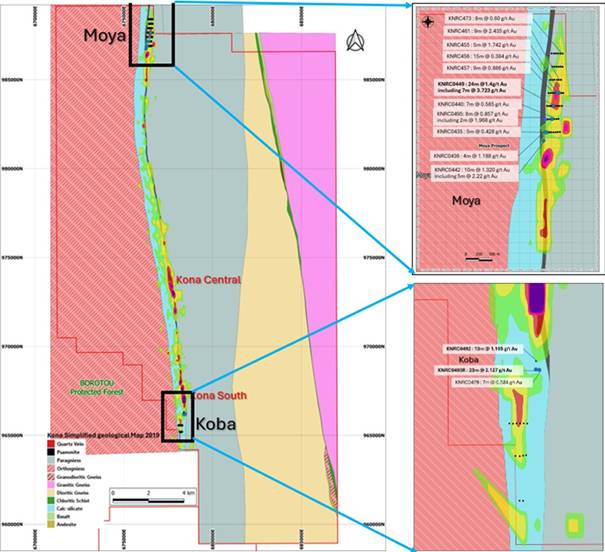

On the Kona permit, 68 RC holes in total 4,196 metres were completed at Moya and Koba prospects, shown in Figure 6, targeting extensions of known mineralised zones at Kona Central and Kona South.

Gold mineralisation is hosted within sheared psammite metasediments and associated with disseminated sulphides predominantly arsenopyrite and minor pyrite and is characterised by silicification, sericite alteration and high-grade zones for further evaluation.

Figure 6: Kona permit location and geology

Results from the majority of the holes completed at Moya and Koba were returned with encouraging intersections from both prospects. Highlights include:

Moya Prospect

• KNRC0442 - 10m @ 1.3g/t Au from 87m

• KNRC0449 - 24m @ 1.4g/t Au from 17m

• KNRC0461 - 9m @ 2.4 g/t Au from 0m

Koba Prospect

• KNRC0493R - 23m @ 2.1 g/t Au from 81m

• KNRC0492 - 13m @ 1.2 g/t Au from 108m

Following these very encouraging initial drill results at Kona, we are excited to announce plans to launch a comprehensive scoping study which will be issued in early H2 2026. This pivotal step is designed to unlock the ABC Project's true value and identify strategic growth opportunities that will benefit the Group and deliver strong returns for our shareholders.

La Debo Project

The La Debo project is in the south of Côte d'Ivoire, approximately 280 km west of Abidjan. In October, Resolute was granted two exploration permits (Okroyou and Serihio) that are adjacent to La Debo.

In November, Resolute announced an Inferred Mineral Resource Estimate for La Debo (G3N and G3S prospects) of 17.6Mt grading 1.14 g/t Au for 643 koz of contained gold at 0.5g/t. Gold mineralisation varies from approximately 10 to 50m in thickness (measured across the zone from hanging wall to footwall) with a strike length of 1.6km for G3N and 1.5km for G3S. The gold mineralisation at G3N and G3S is from surface with consistent grades along strike and downdip. The Mineral Resources at the G3N and G3S prospects remain open down dip with grades encountered so far increasing at depth at G3S.

La Debo Mineral Resource Estimate | |||

Classification | Tonnes | Grade (g/t Au) | Ounces (Au) |

G3N (Inferred) | 8,580,000 | 0.94 | 259,000 |

G3S (Inferred) | 8,978,000 | 1.33 | 384,000 |

Total | 17,559,000 | 1.14 | 643,000 |

Table 5: La Debo Mineral Resources at November 2025 (0.5g/t cut off)

In parallel with the drilling program at G3N and G3S, an auger drilling program has been completed over the south-western half of the permit to define targets where surface geochemistry is erratic. A strong gold anomaly has been confirmed at the G1 prospect area and will be drill tested in early 2026.

Building on the updated MRE at La Debo and the promising drill results at depth at G3S, we intend to carry out a scoping study, which is scheduled for release in the second half of 2026. This will enable the Company to evaluate the potential of La Debo and identify strategic avenues for growth in the region.

Financial Highlights and Balance Sheet Activities

2025 Net Cash Movements (US$ million)

Quarterly Net Cash Movements (US$ million)

In Q4 gold sales of 49,941 oz were achieved at an average realised gold price of $4,023/oz (Q3:

$3,404/oz), with all gold being sold at spot prices. The strong gold price environment helped the Company generate an operating cashflow of $85.7 million in Q4.

The VAT paid in Q4 in Mali and Senegal was $13.5 million (Q3: $20.1 million). During the Quarter $2.7 million of VAT mandates were issued by the Senegalese tax authorities and were used to settle payables. Resolute continues to engage with local governments to settle these amounts. The working capital inflow of $29.0 million in Q4 was attributable to the reduction of stockpiles related to Mako of $10.0 million, a reduction in consumable inventory across both Syama and Mako of approximately $6.0 million, with the remainder due to the timing of supplier payments which are settled in the normal course of business. At the end of December there was $134.6 million of bullion on hand that was sold in January 2026.

EBITDA for the twelve months ending 31 December 2025 was $382.9 million (2024: $287.6 million) driven by $865.6 million of revenue (2024: $664.1 million) driven by the increase in gold price over the year.

Exploration Expenditure

Total Group exploration spend in Q4 was $5.6 million (Q3 2025: $8.8 million), with drilling programs continuing in Senegal, Mali and Côte d'Ivoire throughout the Quarter. The split of the expenditure across the countries in Q4 mainly consist of drilling oxides on the Finkolo Permit in Mali ($0.2 million), Tomboronkoto studies and Bantaco drilling in Senegal ($4.0 million) and drilling at La Debo in Côte d'Ivoire ($0.6 million).

Exploration spend for the full year was $24.1 million which is in line with full year guidance of $20 - $25 million.

Net Cash Summary

Net cash at 31 December 2025 was $209.1 million, increasing from the $136.6 million net cash position at 30 September 2025.

Total borrowings at 31 December 2025 were $57.0 million (Q3 2025: $31.6 million) which includes in-country overdraft facilities in Mali and Senegal of $45.8 million, used to optimise working capital, as well as $11.2 million for in-country equipment financing. Cash, cash equivalents and bullion increased by

$97.8 million in the Quarter to $266.0 million (Q3: $168.2 million). The Company has available liquidity of over $322.3 million (including $134.6 million bullion on hand) as at 31 December 2025.

Financing Updates

Resolute intends to use its existing balance sheet to progress Doropo into construction which is expected in H1 2026. The Company continues to generate robust cash flows from its operations and at the end of Q4 2025 had a net cash position of $209.1 million.

The Company is actively considering a range of funding options to support the construction of the Doropo project.

2026 Guidance

For 2026 Resolute expects total Group gold production of 250,000 - 275,000 oz at an AISC of $2,000 - 2,200/oz (at a gold price assumption of $4,000/oz). For every $100/oz increase in gold price we anticipate a $20/oz increase in Group AISC.

Total Group capital expenditure, inclusive of Doropo and exploration, is expected to be between $310 - 360 million in 2026. Administration and other corporate expenditure is expected to be approximately

$25 million.

Syama Guidance

The Company is providing 2026 production guidance of 195,000 - 210,000 oz at an AISC of $1,950 - 2,150/oz (at a gold price of $4,000/oz). Production for Syama sulphide and oxide is expected to be 180,000 - 190,000 oz and 15,000 - 20,000 oz respectively.

Before commissioning of the SSCP the plan is to continue to process oxide material throughout Q1. The SSCP will be commissioned in two stages first at a 50% capacity then at 100% capacity.

Stage 1 of the SSCP will be commissioned at the start of Q2 to match the availability of high-grade sulphide ore from Syama North (A21). Initially, the SSCP circuit will run at 50% capacity until the

|

2 subject to receiving FID by end of Q1 2026

secondary crushing circuit and ball mill are online. During Q3, with completion of the ball mill and secondary crushing circuit, stage 2 will be commissioned. From this point, the SSCP circuit will be able to fully process sulphide material as well as maintain flexibility to switch between sulphide and oxides.

In 2026 at Syama, production guidance is underpinned by a consistent approach across both underground and open pit operations.

Underground mining is expected to maintain a steady output of approximately 2.6 Mt in 2026, with grades ranging between 2.4 - 2.5 g/t, providing a stable sulphide feed.

In the open pit activities there will be oxide and sulphide ore being mined. Approximately 1 Mt of sulphide ore will be mined from the Syama North (A21) open pit with production 70% weighted towards H2. This material will proved the initial feed to the SSCP. Open pit oxide ore production is being strategically phased with the SSCP commissioning. Overall, 0.3 Mt of oxide ore will be mined in 2026 with 70% in Q2. The open pit strip ratio (oxide and sulphide) is anticipated to be approximately 10:1.

In 2026 there will be approximately of 0.7 Mt of oxide material being processed through the SSCP plant. This comprises a blend of stockpiles and mined ore with the blended head grade averaging 1 g/t. In Q1, prior to SSCP commissioning, oxide stockpiles will be processed. In Q4 once the SSCP is fully commissioned a two-month campaign treating higher grade oxide material is planned.

Across the existing sulphide plant and SSCP there is expected to be c. 2.9 Mt of sulphide material processed at a head grades between 2.5 - 2.6 g/t. In Q2 there is a planned plant shutdown to tie in the SSCP and upgrade the roaster. As a result we expect lower sulphide production in Q2.

Throughout 2026, the Company plans to constantly update and optimise the operational plan at Syama particularly the balance between oxide and sulphide production once the SSCP is operational. This approach positions the Company well to meet production objectives at Syama.

Beyond 2026, with the SSCP operating at a steady state we would expect annual production to be 5-10% higher than in 2026. Oxide gold production is expected to drop over the next couple of years as the operation transitions to predominantly sulphide processing.

In the second half of 2026 the Company is planning to release optimization studies to further increase the throughput at Syama which will be subject to improvements in the geopolitical environment.

Total capital expenditure at Syama in 2025 is expected to be $110 - 125 million. Sustaining capital expenditure includes approximately $30 million of waste stripping at Syama North A21 pits which will provide higher grade sulphide material helping drive the 5-10% uplift in production. There is approximately $40 million of remaining expenditure for the SSCP (non-sustaining).

Mako Guidance

Production at Mako for 2026 is expected to be 55,000 - 65,000 oz at an AISC of $1,600 - 1,800/oz (at a gold price of $4,000/oz).

The Mako plant is scheduled to process c. 2.2 Mt of stockpile material at an average grade and recovery of approximately 0.9 g/t and 90% respectively. Gold production expected to be steady throughout 2026 although variability in stockpile grades is possible. Stockpile processing will continue through to the end of 2027 at similar production levels to 2026.

Total capital expenditure in 2026 at Mako is expected to be approximately $5 million comprised of general sustaining capital expenditure.

The Company is aiming to extend the Mako mine with the MLEP that consists of the two satellite deposits Tomboronkoto and Bantaco. The Company expects to spend $10 - 15 million on the MLEP in 2026. This will be to progress engineering studies, RAP workstreams, equipment procurement and early works once permits are awarded.

Exploration

Exploration is central to Resolute's strategy, supporting our goal of sustained growth, building a robust diversified pipeline of project and long-term shareholder value. Therefore, in 2026 the exploration budget across the Group is $15-25 million with the majority being capital expenditure.

In Mali, approximately $4 million is allocated for deeper drilling of the sulphides at Syama North.

In Senegal, approximately $5 - 8 million has been budgeted for exploration. The funds will be used to drill test the identified gold targets on the Laminia and Sangola permits as well as an allocation for extensional drilling of the Mineral Resources on the Bantaco permit.

In Cote d'Ivoire, over $10 million is budgeted for 2026 to advance the ABC and La Debo projects.

Exploration on the ABC Project in 2026 will concentrate on expanding the existing Mineral Resource base of 2.2 Moz at Kona North and South deposits. Drilling programs will be undertaken on the Kona on targets along strike to the north of the Kona deposits. A total of 2,000m of diamond drilling and 3,000m of RC drilling is planned to test the extensions of the mineralized envelope of the Mineral Resources. A Scoping Study to evaluate the existing Kona Mineral Resources is planned and is expected in early H2 2026.

Drilling programs will also be undertaken on the Farako-Nafana and the Gbemanzo permits. On the Farako-Nafana permit follow up drilling is planned at the Yele Prospect. In Q1, on the Gbemanzo permit a first phase of drilling (1,000m diamond and 3,000m RC drilling) is planned to start in order to test the recently identified strong surface gold anomalies.

Exploration at La Debo will be focused on extending the high-grade mineralisation intersected at G3S. Diamond drilling to test the G3S high-grade extensions is planned to start during the first half of 2026 with 3,500m of drilling planned in the initial follow up phase.

An extensive auger drilling program has been completed over the south-western half of the La Debo permit to define targets where surface geochemistry is erratic. This has confirmed a strong gold anomaly at the G1 prospect area which will be drill tested in early 2026. A Scoping Study to evaluate La Debo is planned and is expected in early H2 2026.

On the newly granted Serihio and Okroyou permits early-stage exploration programs will commence in 2026.

In Guinea, Resolute plans to restart exploration activities in 2026. The Company has received a first reconnaissance authorisation covering 83 km2within the Siguiri Basin, west of Bankan town. Other licences are expected to be granted during the year.

Contact

Resolute

Matthias O'Toole Howes,

Corporate Development and Investor Relations Manager

Matthias.otoolehowes@resolutemining.com

+44 203 3017 620

Public Relations

Jos Simson, Tavistock resolute@tavistock.co.uk

+44 207 920 3150

Corporate Brokers

Jennifer Lee, Berenberg

+44 20 3753 3040

Tom Rider, BMO Capital Markets

+44 20 7236 1010

About Resolute

Resolute is an African-focused gold miner with more than 30 years of experience as an explorer, developer and operator. Throughout its history the Company has produced more than 9 million ounces of gold from ten gold mines. The Company is now entering a growth phase through the development of the Doropo project in Côte d'Ivoire which will supplement the existing production from the Syama mine in Mali and Mako mine in Senegal.

Through all its activities, sustainability is the core value at Resolute. This means that protecting the environment, providing a safe and productive working environment for employees, uplifting host communities, and practicing good corporate governance are non-negotiable priorities. Resolute's commitment to sustainability and good corporate citizenship has been cemented through its adoption of and adherence to the Responsible Gold Mining Principles (RGMPs). This framework, which sets out clear expectations for consumers, investors, and the gold supply chain as to what constitutes responsible gold mining, is an initiative of the World Gold Council of which Resolute has been a full member since 2017. The Company was audited as conformant with these RGMPs in 2024.

Appendix 1

Q4 Production and Costs (unaudited)

December 2025 - Quarter to date |

Units | Syama Sulphide |

Syama Oxide |

Syama |

Mako | Group Total |

UG Lateral Development | m | 440 | - | 440 | - | 440 |

UG Vertical Development | m | - | - | - | - | - |

Total UG Development | m | 440 | - | 440 | - | 440 |

UG Ore Mined | t | 708,404 | - | 708,404 | - | 708,404 |

UG Grade Mined | g/t | 2.21 | - | 2.21 | - | 2.21 |

OP Operating Waste | BCM | 17,614 | 1,125,980 | 1,143,594 | - | 1,143,594 |

OP Ore Mined | BCM | 1,408 | 69,097 | 70,505 | - | 70,505 |

OP Grade Mined | g/t | 1.09 | 1.83 | 1.81 | - | 2.14 |

Total Ore Mined | t | 711,984 | 146,486 | 858,470 | - | 858,470 |

Total Tonnes Processed | t | 582,931 | 394,486 | 977,417 | 603,698 | 1,581,115 |

Grade Processed | g/t | 2.34 | 1.02 | 1.81 | 1.04 | 1.51 |

Recovery | % | 78 | 81 | 79 | 91 | 84 |

Gold Recovered | oz | 34,121 | 10,514 | 44,635 | 18,352 | 62,987 |

Gold in Circuit Drawdown/(Addition) | oz | 1,877 | 651 | 2,528 | 403 | 2,931 |

Gold Produced (Poured) | oz | 35,998 | 11,165 | 47,163 | 18,755 | 65,918 |

Gold Sold | oz | 18,861 | 11,165 | 30,026 | 19,915 | 49,941 |

Achieved Gold Price | $/oz | - | - | - | - | 4,023 |

Cost Summary | ||||||

Mining | $/oz | 617 | 837 | 669 | 216 | 540 |

Processing | $/oz | 719 | 996 | 785 | 677 | 754 |

Site Administration | $/oz | 196 | 329 | 227 | 369 | 267 |

Site Operating Costs | $/oz | 1,532 | 2,162 | 1,682 | 1,261 | 1,562 |

Royalties | $/oz | 464 | 459 | 463 | 234 | 401 |

By-Product Credits | $/oz | (4) | (4) | (4) | - | 124 |

Total Cash Operating Costs | $/oz | 1,992 | 2,616 | 2,141 | 1,495 | 2,086 |

Sustaining Capital | $/oz | 60 | - | 46 | 16 | 37 |

Inventory Adjustments | $/oz | (105) | (1,378) | (407) | 155 | (247) |

All-In Sustaining Cost (AISC) AISC is calculated on gold produced (poured) |

$/oz |

1,947 |

1,239 |

1,779 |

1,666 |

1,877 |

Year-to-date 2025 Production and Costs (unaudited)

December 2025 - Year to date |

Units | Syama Sulphide | Syama Oxide |

Syama |

Mako | Group Total |

UG Lateral Development | m | 3,520 | - | 3,520 | - | 3,520 |

UG Vertical Development | m | 73 | - | 73 | - | 73 |

Total UG Development | m | 3,593 | - | 3,593 | - | 3,593 |

UG Ore Mined | t | 2,158,581 | - | 2,158,581 | - | 2,158,581 |

UG Grade Mined | g/t | 2.32 | - | 2.32 | - | 2.32 |

OP Operating Waste | BCM | 75,884 | 5,474,665 | 5,550,549 | 566,066 | 6,116,615 |

OP Ore Mined | BCM | 22,812 | 421,760 | 444,572 | 448,893 | 893,465 |

OP Grade Mined | g/t | 1.34 | 1.53 | 1.52 | 1.91 | 1.72 |

Total Ore Mined | t | 2,205,297 | 803,650 | 3,008,947 | 1,242,013 | 4,250,960 |

Total Tonnes Processed | t | 2,360,251 | 1,568,595 | 3,928,846 | 2,280,986 | 6,209,832 |

Grade Processed | g/t | 2.25 | 0.98 | 1.74 | 1.49 | 1.65 |

Recovery | % | 77 | 82 | 78 | 92 | 83 |

Gold Recovered | oz | 130,304 | 40,434 | 170,738 | 100,657 | 271,395 |

Gold in Circuit Drawdown/(Addition) | oz | 5,132 | 471 | 5,603 | 238 | 5,841 |

Gold Produced (Poured) | oz | 135,436 | 40,905 | 176,341 | 100,895 | 277,236 |

Gold Bullion in Metal Account Movement (Increase)/Decrease | oz | (15,656) | - | (15,656) | (3,036) | (18,692) |

Gold Sold | oz | 119,780 | 40,905 | 160,685 | 97,859 | 258,544 |

Achieved Gold Price | $/oz | - | - | - | - | 3,338 |

Cost Summary | ||||||

Mining | $/oz | 538 | 745 | 586 | 248 | 463 |

Processing | $/oz | 674 | 1,047 | 761 | 517 | 672 |

Site Administration | $/oz | 183 | 358 | 224 | 185 | 210 |

Site Operating Costs | $/oz | 1,395 | 2,150 | 1,571 | 950 | 1,345 |

Royalties | $/oz | 397 | 391 | 396 | 181 | 320 |

By-Product Credits | $/oz | (4) | (4) | (4) | - | 100 |

Total Cash Operating Costs | $/oz | 1,788 | 2,537 | 1,963 | 1,131 | 1,765 |

Sustaining Capital + Others | $/oz | 123 | 270 | 157 | 29 | 110 |

Inventory Adjustments | $/oz | 45 | (626) | (111) | 109 | (32) |

All-In Sustaining Cost (AISC) per ounce poured | $/oz | 1,956 | 2,181 | 2,009 | 1,269 | 1,843 |

ASX Listing Rule 5.23 Mineral Resources

This announcement contains estimates of Resolute's mineral resources. The information in this Quarterly report that relates to the mineral resources of Resolute has been extracted from reports entitled 'Ore Reserves and Mineral Resource Statement' announced on 11 March 2025, 'Initial Mineral Resource at Bantaco' announced on 24 July 2025, 'Doropo Mineral Resource Update' announced on 8 September 2025, 'Initial Mineral Resource at La Debo' announced 18 November 2025 and are available to view on Resolute's website (www.rml.com.au) and www.asx.com (Resolute Announcement).

For the purposes of ASX Listing Rule 5.23, Resolute confirms that it is not aware of any new information or data that materially affects the information included in the Resolute Announcement and, in relation to the estimates of Resolute's ore reserves and mineral resources, that all material assumptions and technical parameters underpinning the estimates in the Resolute Announcement continue to apply and have not materially changed. Resolute confirms that the form and context in which the Competent Person's findings are presented have not been materially modified from that announcement.

ASX Listing Rule 5.19 Production Targets

The information in this announcement that relates to production targets of Resolute has been extracted from the report entitled 'Q4 2025 Activities Report and 2026 Guidance' announced on 22 January 2026 and are available to view on the Company's website (www.rml.com.au) and www.asx.com (Resolute Production Announcement).

For the purposes of ASX Listing Rule 5.19, Resolute confirms that all material assumptions underpinning the production target, or the forecast financial information derived from the production target, in the Resolute Production Announcement continue to apply and have not materially changed.

Cautionary Statement about Forward-Looking Statements

This announcement contains certain "forward-looking statements" including statements regarding our intent, belief, or current expectations with respect to Resolute's business and operations, market conditions, results of operations and financial condition, and risk management practices. The words "likely", "expect", "aim", "should", "could", "may", "anticipate", "predict", "believe", "plan", "forecast" and other similar expressions are intended to identify forward-looking statements. Indications of, and guidance on, future earnings, anticipated production, life of mine and financial position and performance are also forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Resolute's actual results, performance and achievements or industry results to differ materially from any future results, performance or achievements, or industry results, expressed or implied by these forward-looking statements. Relevant factors may include (but are not limited to) changes in commodity prices, foreign exchange fluctuations and general economic conditions, increased costs and demand for production inputs, the speculative nature of exploration and project development, including the risks of obtaining necessary licences and permits and diminishing quantities or grades of reserves, political and social risks, changes to the regulatory framework within which Resolute operates or may in the future operate, environmental conditions including extreme weather conditions, recruitment and retention of personnel, industrial relations issues and litigation.

Forward-looking statements are based on Resolute's good faith assumptions as to the financial, market, regulatory and other relevant environments that will exist and affect Resolute's business and

operations in the future. Resolute does not give any assurance that the assumptions will prove to be correct. There may be other factors that could cause actual results or events not to be as anticipated, and many events are beyond the reasonable control of Resolute. Readers are cautioned not to place undue reliance on forward-looking statements, particularly in the significantly volatile and uncertain current economic climate. Forward-looking statements in this document speak only at the date of issue. Except as required by applicable laws or regulations, Resolute does not undertake any obligation to publicly update or revise any of the forward-looking statements or to advise of any change in assumptions on which any such statement is based. Except for statutory liability which cannot be excluded, each of Resolute, its officers, employees and advisors expressly disclaim any responsibility for the accuracy or completeness of the material contained in these forward-looking statements and excludes all liability whatsoever (including in negligence) for any loss or damage which may be suffered by any person as a consequence of any information in forward-looking statements or any error or omission.

Competent Persons Statement

The information in this report that relates to the Exploration Results, Mineral Resources and Ore Reserves is based on information compiled by Mr Bruce Mowat, a member of The Australian Institute of Geoscientists. Mr Bruce Mowat has more than 15 years' experience relevant to the styles of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person, as defined in the 2012 Edition of the "Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves" (the JORC Code). Mr Bruce Mowat is a full-time employee of the Resolute Mining Limited Group and holds equity securities in the Company. He has consented to the inclusion of the matters in this report based on his information in the form and context in which it appears. This information was prepared and disclosed under the JORC Code 2012 except where otherwise noted.

Appendix 2. Recent drilling results

HoleID | East (WGS) | North (WGS) | RL | EOH(m) | DIP | AZI (WGS) | From (m) | To (m) | Width (m) | Au g/t |

FNRC0021 | 668294 | 1022274 | 430 | 55 | -55 | 90 | 29 | 36 | 7 | 1 |

FNRC0027 | 668415 | 1022071 | 436 | 55 | -55 | 90 | 39 | 53 | 14 | 1 |

FNRC0036 | 668286 | 1022530 | 422 | 39 | -55 | 90 | 16 | 19 | 3 | 1 |

FNRC0111 | 661159 | 1028573 | 430 | 57 | -55 | 55 | 13 | 33 | 20 | 3 |

FNRC0111 | 661159 | 1028573 | 430 | 57 | -55 | 55 | 39 | 44 | 5 | 2 |

KNRC0435 | 676318 | 986900 | 381 | 66 | -55 | 90 | 38 | 41 | 3 | 1 |

KNRC0436 | 676280 | 986903 | 381 | 114 | -55 | 90 | 82 | 86 | 4 | 1 |

KNRC0440 | 676416 | 987152 | 376 | 54 | -55 | 90 | 48 | 53 | 5 | 1 |

KNRC0442 | 676253 | 986739 | 383 | 114 | -55 | 90 | 89 | 96 | 7 | 2 |

KNRC0449 | 676443 | 987401 | 378 | 54 | -55 | 90 | 17 | 24 | 7 | 1 |

KNRC0449 | 676443 | 987401 | 378 | 54 | -55 | 90 | 28 | 41 | 13 | 2 |

KNRC0455 | 676551 | 987650 | 390 | 54 | -55 | 90 | 13 | 18 | 5 | 2 |

KNRC0456 | 676510 | 987650 | 390 | 54 | -55 | 90 | 52 | 58 | 6 | 1 |

KNRC0457 | 676469 | 987649 | 389 | 54 | -55 | 90 | 15 | 24 | 9 | 1 |

KNRC0461 | 676585 | 987900 | 389 | 54 | -55 | 90 | 3 | 8 | 5 | 4 |

KNRC0473 | 676615 | 988399 | 386 | 54 | -55 | 90 | 16 | 24 | 8 | 1 |

KNRC0476 | 676491 | 988402 | 390 | 54 | -55 | 90 | 25 | 29 | 4 | 1 |

KNRC0479 | 678426 | 966177 | 388 | 75 | -55 | 90 | 66 | 72 | 6 | 1 |

KNRC0480 | 678241 | 964685 | 351 | 54 | -55 | 90 | 8 | 11 | 3 | 1 |

KNRC0481 | 678202 | 964686 | 350 | 54 | -55 | 90 | 48 | 51 | 3 | 1 |

KNRC0492 | 678389 | 966277 | 389 | 123 | -55 | 90 | 108 | 121 | 13 | 1 |

KNRC0493R | 678387 | 966182 | 388 | 130 | -55 | 90 | 81 | 104 | 23 | 2 |

Notes to Accompany Table:

• Grid coordinates are WGS84 Zone 29 North

• RC intervals are sampled every 1m by dry riffle splitting or scoop to provide a 2-3kg sample

• Cut-off grade for reporting of intercepts is >0.5g/t Au with a maximum of 3m consecutive internal dilution included within the intercept; only intercepts >=3m and no restriction of gram x metres are reported

• Recent drill samples are analysed for gold by MSA Labs CPA-Au1 500g sample gamma ray analysis by photon assay instrument

JORC Code, 2012 Edition - Table 1 report Section 1 Sampling Techniques and Data ABC Project

Criteria | JORC Code explanation | Commentary |

Sampling techniques | • Nature and quality of sampling (eg cut channels, random chips, or specific specialised industry standard measurement tools appropriate to the minerals under investigation, such as down hole gamma sondes, or handheld XRF instruments, etc). These examples should not be taken as limiting the broad meaning of sampling. • Include reference to measures taken to ensure sample representivity and the appropriate calibration of any measurement tools or systems used. • Aspects of the determination of mineralisation that are Material to the Public Report. • In cases where 'industry standard' work has been done this would be relatively simple (eg 'reverse circulation drilling was used to obtain 1 m samples from which 3 kg was pulverised to produce a 30 g charge for fire assay'). In other cases more explanation may be required, such as where there is coarse gold that has inherent sampling problems. Unusual commodities or mineralisation types (eg submarine nodules) may warrant disclosure of detailed information. | • The sampling was conducted using multiple techniques tailored to the project's geological and surface conditions. A systematic rock sampling program was caried out in 2017 to fully characterise the surface expression of the mineralisation. A total of 788 rock samples were collected in 2017 and 205 rock samples in 2019/2020. • Auger drilling was employed extensively over the mineralised corridor to adequately characterise the underlying rocks. Auger drilling recovered material systematically for gold analysis and geochemical interpretation. As with the rock chips, auger samples were analysed for Au by fire assay with AAS finish at Bureau Veritas in Abidjan. Multi-element analyses were completed by four-acid digest with ICP-AES and ICP-MS finish at ACME Laboratories in Vancouver. A total of 2,843 samples were collected at the end of 2020 from 22,219m drilled. • Reverse Circulation (RC) and Diamond Core (DD) drilling were the principal methods used for delineating Mineral Resources. RC drilling was conducted using 5¼ to 5¾ inch diameter face-sampling hammers to recover one-metre interval samples, typically dry unless groundwater was encountered. Diamond drilling employed HQ and NQ diameter core, with triple tube techniques for improving recovery in broken ground. RC samples were riffle split on site, and core samples were sawn to produce half-core for analysis. Sampling procedures incorporated QAQC measures, including the insertion of blanks, standards, and duplicates to ensure sample representivity. Assay protocols utilised 50 g fire assay (AAS finish) for gold, and multi-element analysis was performed where applicable. |

Drilling techniques | • Drill type (eg core, reverse circulation, open-hole hammer, rotary air blast, auger, Bangka, sonic, etc) and details (eg core diameter, triple or standard tube, depth of diamond tails, face-sampling bit or other type, whether core is oriented and if so, by what method, etc). | • Drilling methods involved a combination of Reverse Circulation (RC), Diamond Core (DD), and auger drilling methods. RC drilling was primarily used for delineating near-surface mineralisation and preliminary resource definition. RC drilling employed face-sampling hammers with bit sizes ranging from 5¼ to 5¾ inches. Dry drilling was the standard procedure, with drilling halted at the water table to prevent contamination from wet samples; below groundwater, diamond drilling methods were applied. • Diamond core drilling used HQ and NQ diameter core. Triple-tube systems were implemented in highly broken ground to maximise core recovery, while standard double-tube setups were used elsewhere. Downhole surveys are taken every 30m with a single shot Reflex EZ shot system. Orientation of diamond core was conducted selectively using Reflex ACT II core orientation devices to facilitate structural logging. Auger drilling was utilised for shallow exploration across the entire area. All drill methods were executed to a high standard with contractors experienced in gold exploration in West Africa. |

Drill sample recovery | • Method of recording and assessing core and chip sample recoveries and results assessed. • Measures taken to maximise sample recovery and ensure representative nature of the samples. • Whether a relationship exists between sample recovery and grade and whether sample bias may have occurred due to preferential loss/gain of fine/ coarse material. | • Drill sample recovery was systematically monitored during both RC and diamond drilling programs. RC samples were weighed regularly, to monitor sample size consistency and ensure the representativeness of samples. Analysis of sample weights of 47,562 RC samples from Kona South and 47,464 RC samples showed a consistent recovery trend stabilizing between 30-40 kg per metre after clearing the uppermost weathered horizons. Minor variations in sample weight were observed at shallow depths and in softer materials; however, statistical checks confirmed no significant bias in gold grade associated with sample mass. • Diamond core recovery was measured, with an overall average recovery of approximately 96% across the project. Recovery rates improved with depth, with 81% core recovery in oxide, 91% recovery in transitional and 99% in fresh. Core recovery measurements were recorded in the database for each run. The use of triple-tube drilling in broken ground contributed to maintaining high recovery standards. The overall conclusion, supported by quality control reviews, was that there is no significant sampling bias attributable to differential recovery. |

Logging | • Whether core and chip samples have been geologically and geotechnically logged to a level of detail to support appropriate Mineral Resource estimation, mining studies and metallurgical studies. • Whether logging is qualitative or quantitative in nature. Core (or costean, channel, etc) photography. • The total length and percentage of the relevant intersections logged. | • Comprehensive geological and geotechnical logging was undertaken for all drillholes including RC and DD. Drillholes were logged systematically for a range of key geological attributes: lithology, alteration, mineralisation, texture, structure, weathering, and rock quality designation (RQD). RC samples were logged visually on site, with geological observations recorded both digitally and on physical log sheets where applicable. Diamond core was logged in greater detail, particularly for structural geology, alteration styles, mineral assemblages, and vein relationships, providing critical inputs for 3D geological modelling. |

• Photographic records were maintained for all diamond drill core - photographed both wet and dry - before sampling. Logging captured sufficient detail to support resource estimation, mining studies, and metallurgical investigations. Logging procedures included the use of a standardised lithological and alteration coding scheme to ensure consistency across the drilling campaigns. Digital capture of logging data into a centralised database with validation rules also enhanced data reliability. |

Sub-sampling techniques and sample preparation | • If core, whether cut or sawn and whether quarter, half or all core taken. • If non-core, whether riffled, tube sampled, rotary split, etc and whether sampled wet or dry. • For all sample types, the nature, quality and appropriateness of the sample preparation technique. • Quality control procedures adopted for all sub-sampling stages to maximise representivity of samples. • Measures taken to ensure that the sampling is representative of the in situ material collected, including for instance results for field duplicate/second-half sampling. • Whether sample sizes are appropriate to the grain size of the material being sampled. | • Systematic sub-sampling and sample preparation protocols were employed to ensure that samples remained representative of in situ mineralisation. For RC drilling, 1 m samples were split on site using a three-tier riffle splitter to achieve a target sample size of approximately 2 to 3 kg for laboratory submission. Wet samples encountered in shallow zones were left to dry naturally prior to splitting where possible. For diamond drilling, core was cut lengthwise using diamond-bladed core saws; half-core samples were collected for routine assay, while the other half was preserved for reference and potential future re-assay. • Sample preparation at the laboratory followed industry best practices. Samples were oven dried, crushed to 70 to 85% passing 2 mm, then riffle split to produce a subsample for pulverisation. The pulverised material was milled to achieve at least 85% passing 75 microns, producing a pulp of approximately 150 to 250 g for fire assay analysis. Quality assurance measures were built into preparation workflows, including the regular inclusion of duplicate splits and check samples. Laboratory facilities used (primarily Bureau Veritas Abidjan, SGS Ouagadougou) operated to ISO 17025 standards, and internal laboratory QAQC reviews were conducted regularly. More recent Au analyses were conducted by Chrysos Photon assay at MSA labs in Yamoussoukro. Laboratory and assay procedures are appropriate for Mineral Resource estimatio |

Quality of assay data and laboratory tests | • The nature, quality and appropriateness of the assaying and laboratory procedures used and whether the technique is considered partial or total. • For geophysical tools, spectrometers, handheld XRF instruments, etc, the parameters used in determining the analysis including instrument make and model, reading times, calibrations factors applied and their derivation, etc. • Nature of quality control procedures adopted (eg standards, blanks, duplicates, external laboratory checks) and whether acceptable levels of accuracy (ie lack of bias) and precision have been established. | • Assay methodologies were based on internationally recognised standards and utilised reputable laboratories. All drill samples were primarily analysed for gold using 50 g fire assay with atomic absorption spectroscopy (AAS) or inductively coupled plasma atomic emission spectroscopy (ICP-AES) finish. In cases where assays exceeded 10 g/t Au, samples were re-analysed using a gravimetric finish to improve accuracy. For some RC and trench samples, particularly those with coarse gold. • Quality control procedures were rigorous. Certified reference materials (standards), field blanks, and field duplicates were inserted into the sample stream at regular intervals - approximately one QAQC sample every 20 to 30 samples. Laboratory duplicates, internal standards, and blanks were also monitored. QAQC data were routinely reviewed to ensure analytical accuracy and precision. Failures (e.g., a standard outside 3 standard deviations) triggered immediate re-assay of sample batches. No significant long-term bias or drift was observed across the assay dataset. Laboratories involved (Bureau Veritas, Abidjan; MSA Yamoussoukro; and SGS, Ouagadougou) are ISO/IEC 17025 accredited, ensuring laboratory practices are consistent with industry best practice. |

Verification of sampling and assaying | • The verification of significant intersections by either independent or alternative company personnel. • The use of twinned holes. • Documentation of primary data, data entry procedures, data verification, data storage (physical and electronic) protocols. • Discuss any adjustment to assay data. | • Verification of sampling and assaying was undertaken through a combination of internal reviews, duplicate analyses, and independent data validation exercises. Field duplicates were collected regularly from RC drilling to monitor sampling precision, with results demonstrating satisfactory repeatability of gold grades. CRMs and blanks were inserted at regular intervals to monitor assay accuracy and contamination. QAQC charts were reviewed continuously by project geologists and external consultants during key drilling campaigns. • The primary assay laboratories (Bureau Veritas and SGS) conducted their own internal QC programs, which were also monitored. Limited twin drilling was conducted, with twin RC holes and DD holes used to verify mineralisation continuity, grade reproducibility, and geological interpretation; results confirmed good spatial reproducibility. While external umpire (secondary lab) assay programs were not routinely undertaken, the performance of primary laboratories and internal QAQC programs were considered satisfactory for the reporting of Mineral Resources. Assay data and logging data were entered digitally into validated databases, and independent audits of the database have been performed during resource estimation reviews. |

Location of data points | • Accuracy and quality of surveys used to locate drill holes (collar and down-hole surveys), trenches, mine workings and other locations used in Mineral Resource estimation. • Specification of the grid system used. • Quality and adequacy of topographic control. | • Drillhole collar locations were surveyed using a combination of differential GPS (DGPS) systems and total station surveying where higher precision was required. The DGPS surveys were conducted by trained field surveyors to ensure location accuracy suitable for Mineral Resource estimation, with horizontal and vertical accuracy generally within ±0.2 m. In areas of rugged topography or logistical difficulty, survey-grade handheld GPS units were temporarily used during initial exploration stages (rock sampling, auger drilling), but were later replaced with DGPS surveys for all critical drill collars. • Elevation data were tied into the Nivellement Général de Côte d'Ivoire (NGCI) vertical datum. A topographic digital terrain model (DTM) was produced using high-resolution satellite imagery and ground-truthing, which was used for resource modelling. Grid systems used were WGS84, Zone 29N for initial exploration and UTM Zone 29N (WGS84 projection) for final resource definition. |

Data spacing and distribution | • Data spacing for reporting of Exploration Results. • Whether the data spacing and distribution is sufficient to establish the degree of geological and grade continuity appropriate for the Mineral Resource and Ore Reserve estimation procedure(s) and classifications applied. • Whether sample compositing has been applied. | • Drilling was conducted on nominal grid spacings appropriate for the level of confidence required for resource estimation. In the main mineralised zones at Kona South and Kona Central RC and diamond drilling was performed on approximately 50 m x 50 m grids with some areas of wider spacing of 50m x 100m. • Outside the main resource areas, reconnaissance and exploration drilling was more broadly spaced at 50 m x 200 m intervals, appropriate for early-stage resource targeting. Data spacing was assessed during Mineral Resource Estimation and was found sufficient to establish geological and grade continuity for inferred classification. No sample compositing was applied prior to resource estimation; raw assay intervals were used directly in estimation procedures. |

Orientation of data in relation to geological structure | • Whether the orientation of sampling achieves unbiased sampling of possible structures and the extent to which this is known, considering the deposit type. • If the relationship between the drilling orientation and the orientation of key mineralised structures is considered to have introduced a sampling bias, this should be assessed and reported if material. | • Drilling programs were designed to target mineralised structures as close to perpendicular as possible to the interpreted dip of mineralisation at each deposit. All drillholes were oriented towards the east with an inclination of -50° to -60°, depending on the local structural orientation of gold-bearing zones. The mineralisation is generally hosted in north trending structures dipping moderately to steeply to the west, making these drill orientations appropriate to intersect mineralised zones at reasonable angles and to minimise bias in the intercept lengths. • Geological interpretations and cross sections confirm that drilling achieved reasonably representative intersections of mineralisation. No significant sampling bias related to drilling orientation was observed during resource modelling and estimation. |

Sample security | • The measures taken to ensure sample security. | • Sample security protocols were implemented to ensure the integrity of all collected samples from the point of collection through to laboratory delivery. After collection, samples were placed into pre-numbered, durable plastic bags and securely sealed. Multiple samples were then packed into larger polyweave sacks for easier handling and protection during transport. Samples were stored in a secure, supervised facility at the exploration camp before transportation. • Transport to the assay laboratories (Bureau Veritas in Abidjan and SGS in Ouagadougou) was carried out either by company personnel or trusted, contracted couriers. Chain-of-custody forms were maintained throughout the transfer process, and receipt of samples was acknowledged in writing by laboratory staff. While rigorous internal controls were observed, there is no specific mention of external audits or independent oversight of sample security protocols. However, no incidents of sample loss, tampering, or contamination have been reported, and laboratory reconciliation of received samples consistently matched dispatch records. |

Audits or reviews | • The results of any audits or reviews of sampling techniques and data. | • Audits and reviews of sampling techniques, assay data, and database integrity have been carried out periodically. Internal technical reviews were performed by Centamin's in-house geology and resource teams throughout the exploration and resource evaluation phases. These reviews covered sampling practices, QAQC data performance, logging standards, and database quality, ensuring consistent application of protocols and identifying areas for procedural improvement where necessary. • Independent reviews of the Resource models and supporting exploration data were conducted as part of the NI 43-101 technical report preparation. Qualified Persons (QPs) signed off on the Mineral Resource estimates after assessing the drilling, sampling, and QAQC procedures. |

Section 2 Reporting of Exploration Results

Criteria | JORC Code explanation | Commentary |

Mineral tenement and land tenure status | • Type, reference name/number, location and ownership including agreements or material issues with third parties such as joint ventures, partnerships, overriding royalties, native title interests, historical sites, wilderness or national park and environmental settings. • The security of the tenure held at the time of reporting along with any known impediments to obtaining a licence to operate in the area. | • The Kona South and Kona Central deposits are the most advanced prospects in Centamin's ABC Kona Project, which is located in the Kabadougou Region of the Denguélé District, in the northwest of Cote D'Ivoire. The Kona permit occurs approximately 600 km west of Centamin's Doropo Project and 540 km north-west of the capital city of Abidjan. The Kona permit is 100% owned by Centamin Cote d'Ivoire SARL, which is a 100% owned Ivoirian subsidiary of Centamin and covers an area of 382.9 km2. • All permits (Kona PR658, Windou PR877 and Farako Nafana) are held in good standing with the Côte d'Ivoire Ministry of Mines and have been maintained in accordance with local legal requirements. There are no known outstanding disputes affecting the licences and no known risks or environmental liabilities that could adversely affect or result in the loss of ownership of the Resource or permits. |

Exploration done by other parties | • Acknowledgment and appraisal of exploration by other parties. | • Newmont are believed to be the first exploration company to explore the area in 2010. They conducted regional drainage sampling, mapping and prospecting across the entire district. This work highlighted the Kona area as one of their highest ranked targets. Local exploration companies, including Golden Oriole and Sani Resources, applied for exploration permits on the back of the Newmont reconnaissance licences but never raised the finance to conduct any significant work and subsequently had their permits revoked. • Centamin acquired the exploration permits from the government in 2015 to 2016. The 2018 Kona South Mineral Resource is the first defined in the area. There is no evidence of any illegal artisanal mining in the permit area. |

Geology | • Deposit type, geological setting and style of mineralisation. | • The ABC Kona project is situated along the main Archean-Birimian Cratonic suture zone in western Côte d'Ivoire, specifically associated with the Sassandra Fault Zone. • The principal mineralised feature identified through mapping and sampling is the Lolosso structure, a north-south striking mineralised zone interpreted as a western splay off the major transcurrent Sassandra Fault. The geological setting includes a narrow keel of later Birimian volcano-sediments entrapped within earlier Archean thrusted granite and gneissic sheets, providing a complex structural and lithological host for mineralisation. • At Kona South, gold is predominantly hosted in psammitic units (north-south striking) dipping approximately 70° west. This unit is sandwiched between a calc-silicate hanging wall to the west and a paragneiss footwall to the east. An additional mafic volcanic unit lies west of the calc-silicate layer, completing the local stratigraphy. • The style of mineralisation is structurally controlled and shows a strong spatial association with arsenopyrite. Arsenopyrite occurs as disseminations and aggregates aligned with the foliation of the psammitic host. Strong silicification is evident within mineralised zones, though quartz veining is rare and does not appear to play a significant role in gold control. |